Gavin Baker vs Leopold Ashenbrenner: The AI Infrastructure Divide

This one came out of the Limitless podcast, where hosts Josh and Ejaaz dig into the competing investment theses of Gavin Baker and Leopold Ashenbrenner. I've pulled apart their analysis because it's the clearest framing I've seen of the AI bubble debate — and the two men sitting on opposite sides of it are both worth taking seriously.

When two of the sharpest macro investors disagree on the same asset class, the disagreement usually reveals something important about how they see risk. Here's my breakdown.

The AI Bubble Debate Has a New Framing

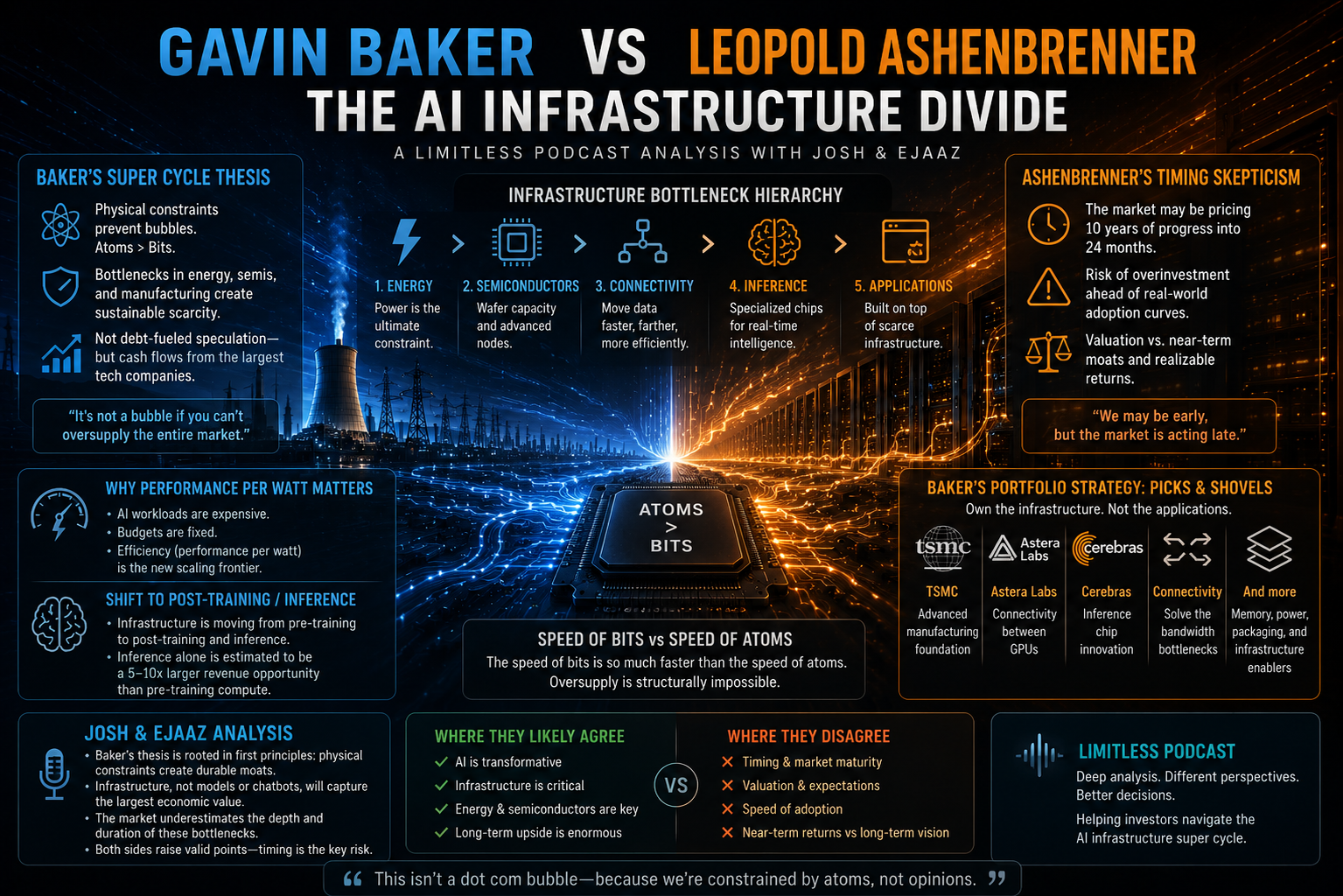

Gavin Baker, founder of Atreides Management with $4.1 billion in assets under management, has been investing in AI infrastructure for over 20 years. His thesis: we're not in a bubble. We're in a super cycle constrained by physical atoms.

Leopold Ashenbrenner, whose previous analysis on infrastructure rotation and momentum exhaustion pointed accurately at regime shifts, sees the same data and draws a different conclusion about timing and conviction.

Baker's Core Thesis: Physical Constraints = No Bubble

Baker's argument is deceptively simple. Bubbles happen when speculative money creates oversupply. The dot-com bubble was debt-fueled speculation that built too much capacity, too fast.

AI is different.

"This isn't a dot-com bubble, because we're not levered on money, but also because the bottlenecks themselves that we're speaking about are constrained by physical atoms."

Here's the critical distinction. In 2000, you could spin up unlimited web servers with borrowed money. Oversupply killed the economics. In 2026, you can't. NVIDIA could sell $2–3 trillion of GPUs this year and next year if only TSMC could supply them. The constraint isn't demand. It's wafers.

"It's not a bubble if you can't oversupply the entire market. We are constrained by the fact that we don't have enough picks and shovels to do the thing."

The picks and shovels aren't software. They're:

- Semiconductor fabrication capacity (TSMC, Samsung)

- Energy infrastructure (watts)

- GPU connectivity (Astera Labs)

- Inference chips (Cerebras)

- Advanced packaging (3D chiplets)

These take years to build. You can't oversupply them. Therefore pricing power persists. Therefore, not a bubble.

The Ashenbrenner Counterpoint: Timing vs Structure

Ashenbrenner's previous macro calls have been prescient on regime shifts. His analysis on commodity supercycles, infrastructure bottlenecks, and momentum exhaustion positioned early and exited at inflection points.

His skepticism on AI isn't that the infrastructure story is wrong. It's that timing and conviction levels matter more than thesis quality when markets are euphoric.

The hosts highlight the tension. Josh: "You can beat Warren Buffett over a year, but can you beat him over multiple decades?"

This isn't about whether Baker's thesis is correct. It's about whether the market is already pricing in the next 10 years of infrastructure buildout in the next 2 years.

Ashenbrenner would likely argue:

- Infrastructure constraints are real, but

- The market already knows about them

- Current valuations assume perfect execution and sustained capex for a decade

- Geopolitical disruption (China, Taiwan, US–China relations) could derail assumptions

- Rotation signals and correlation breakdowns suggest the consensus trade is crowded

Baker's Portfolio: Where the Real Returns Live

Baker isn't betting on ChatGPT or frontier models. Those are already priced. His thesis focuses on four areas where infrastructure constraints create sustained opportunity.

1. Verticalized small language models. Specialized models that optimize for specific tasks, reducing pre-training costs and shifting compute toward inference — where demand is 5–10x larger than pre-training.

2. Sovereign infrastructure deployment. Countries and corporations building their own AI infrastructure to avoid US dependency. Multiple parallel infrastructure stacks equals sustained demand.

3. Performance per watt. "Companies are increasingly caring about how many tokens you can generate per watt." Microsoft and Uber announced they're reducing AI API exposure because their annual budgets got consumed in 4 months. Cost efficiency becomes the limiting factor, not capability — which drives demand for inference-optimized chips and efficiency-first architecture.

4. Energy and space solutions. The real bottleneck isn't GPUs anymore. It's power. Data centers are power-constrained. That creates opportunities in nuclear, renewable energy, and advanced cooling.

The Infrastructure Hierarchy of Returns

Baker's framing of where returns cluster is radical for the AI consensus:

"The biggest returns that you can get in AI is in electricity, power, and silicon fabrication. It's got nothing to do with SaaS software as a service. It's got nothing to do with chatbots, such as Anthropic or OpenAI."

This positions the value chain inverted from how most people think about it.

Highest returns:

- Energy infrastructure (nuclear, renewable)

- Semiconductor fabrication (TSMC, Samsung, Intel foundry)

- GPU connectivity and packaging (Astera Labs, NVIDIA, Broadcom)

- Inference chips (Cerebras, Graphcore)

Medium returns:

- GPU manufacturing (NVIDIA, AMD)

- Memory (Micron, SK Hynix)

- Data center operators (hyperscalers)

Lowest returns:

- AI applications (frontier models, chatbots)

- AI software (most SaaS companies claiming AI)

- Specialized vertical AI

This isn't controversial inside investing circles. But it contradicts the consensus narrative that frontier model companies — OpenAI, Anthropic — are where the value accrues.

Where Baker and Ashenbrenner Might Actually Agree

Both investors recognize:

- Infrastructure bottlenecks are real — physical constraints prevent oversupply

- Pre-training is becoming commoditized — the shift to post-training and inference is structural

- Efficiency matters more each quarter — performance per watt is becoming the metric that drives investment

- Geopolitics reshapes infrastructure — sovereign deployment and US–China dynamics create parallel stacks

- Energy is the final bottleneck — not chips, not wafers, but power

The disagreement isn't about what's true. It's about timing (is this a 2-year transition or a 10-year buildout?), valuations (are current prices assuming 5 years of returns over 24 months?), and correlation risk (what happens if growth assumptions crack and correlations reverse?).

What the Limitless Hosts Highlight

Josh and Ejaaz bring clarity to the framework. Infrastructure constraints are real, but "the speed of bits is so much faster than the speed of atoms."

This means software can scale infinitely — problems solved in weeks. Physical infrastructure takes years: fab capacity, power grids, connectivity. That creates a valley of opportunity for infrastructure investors. But valuations can overshoot the actual constraint-relief timeline.

The hosts essentially bridge the two theses: Baker's infrastructure thesis is sound, but Ashenbrenner's skepticism on timing and conviction levels is worth taking seriously.

The Bottom Line

Gavin Baker argues we're in a sustained super cycle constrained by physical limitations that prevent bubbles. The infrastructure opportunity is decades-long.

Leopold Ashenbrenner would agree on the structure but question whether the market is pricing in a decade of growth over the next 24 months.

The smart positioning: believe Baker's infrastructure thesis, but use Ashenbrenner's timing discipline.

Infrastructure investments will win over time. But correlation breakdowns, momentum exhaustion, and geopolitical disruption suggest the consensus crowd is overextended right now. The picks and shovels Baker identifies will be essential. The question is whether you buy them here or wait for a reset.

Lisa Tamati reports on AI investment strategy, infrastructure, and macro cycles at PTLsignal.com

// newsletter

Want more like this?

Join the PTL Signal newsletter. Weekly AI, Bitcoin & market analysis from Lisa Tamati.