John Tinsman & Marty Bent: The Compute Leasing Economy Just Broke Monetary Policy

Lisa Tamati reporting on John Tinsman and Marty Bent's analysis of compute leasing economics and the breakdown of the Fed's monetary policy transmission.

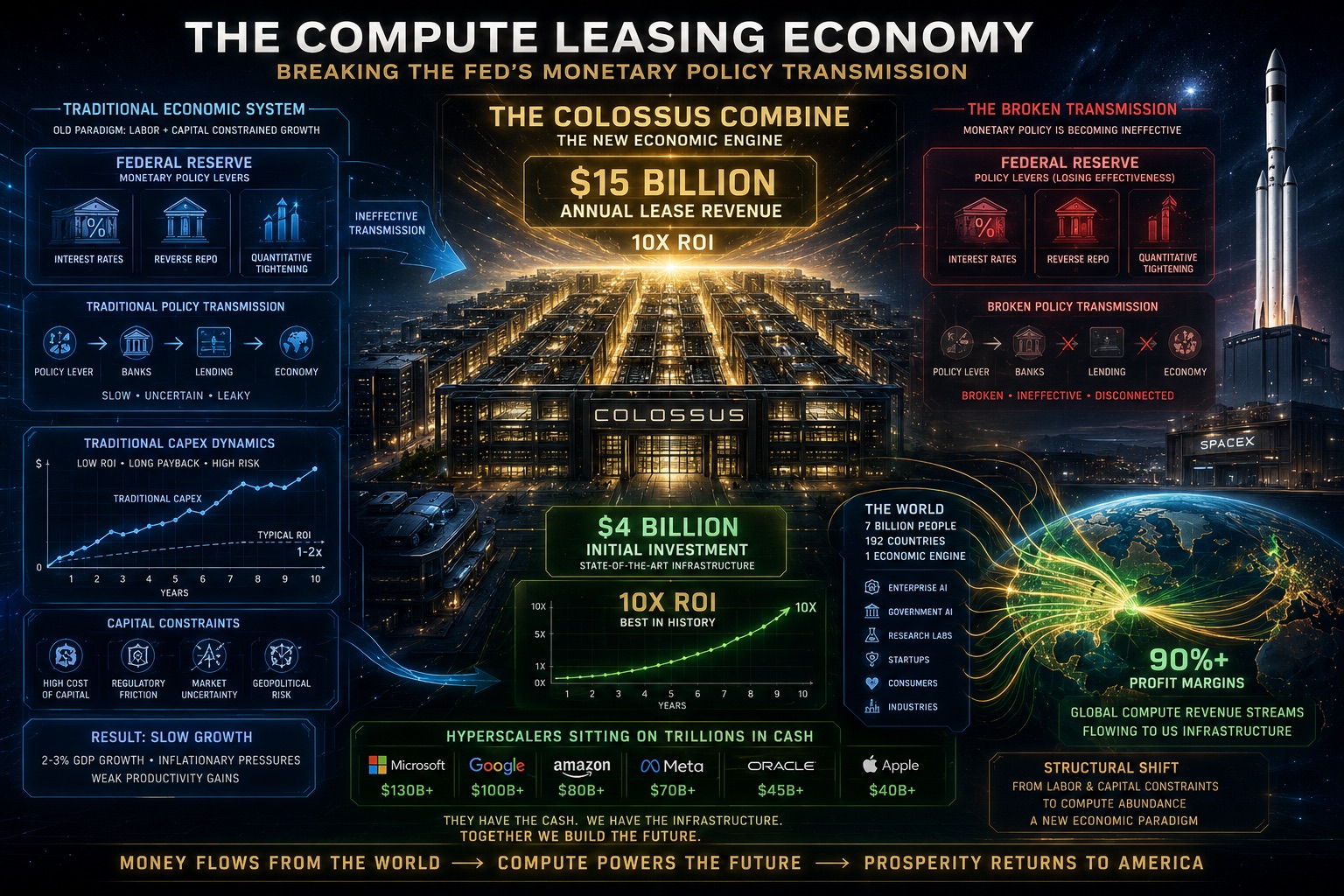

The Fed's Transmission Mechanism Is Broken. And We Just Figured Out Why.

John Tinsman and Marty Bent are discussing something that explains why the Fed's interest rate policy isn't working the way it's supposed to.

The answer: When your biggest capex spenders are generating 100%+ returns on investment and sitting on $800B+ in cash reserves, they don't care what the Fed does.

Here's how we got here.

The Compute Leasing ROI That Should Shock Everyone

Tinsman presents a number that should've dominated financial media but didn't:

XAI is paying $15 billion per year to lease Colossus, a data center that cost $4 billion to build.

Do the math:

- $4 billion investment

- $15 billion annual lease payment

- 3-year lease term = $45 billion total revenue

- 10x return on investment

"They spent 3 to 4 billion... and they lease it to XAI for $15 billion a year for 3 years, it will make $45 billion on a $4 billion investment. So that's a 10x ROI."

This isn't theoretical. This is deployed capital generating returns that would make venture capital funds jealous.

And it's just the beginning.

Colossus 2: $300 Billion on a $17 Billion Bet

SpaceX is planning Colossus 2, a larger facility with a $17 billion build cost.

If Colossus 1 generates 10x returns, what does Colossus 2 look like?

"SpaceX is going to build another large data center Colossus 2... 17 billion outlay... if they only spend 17 billion, it sounds like they could lease that out for over 300 billion."

$300 billion in revenue on a $17 billion investment.

That's 18x ROI on the capital expenditure.

These aren't edge cases. These are the unit economics of compute leasing at scale.

The Token Demand Explosion

The demand side is equally important as the unit economics.

Anthropic grew token sales 80x in just 12 months.

Goldman Sachs projects another 24x growth ahead.

"Token demand grew 80x at Anthropic in 12 months with Goldman projecting another 24x growth ahead."

What this means: The demand for AI compute isn't cyclical. It's exponential.

And the supply is constrained by physics—you can't build data centers faster than you can build them.

This creates pricing power and justifies the 10x+ ROI economics.

Why the Fed Is Irrelevant (For Now)

This is where Tinsman's argument gets dangerous for traditional monetary policy.

The Fed raises rates to slow capex spending and inflation.

But if you're a hyperscaler with a 100%+ ROI project, what do you do?

"If the Fed raises rates 1 or 2% and your ROI is 100%, do you even care?"

You don't. You borrow at 5-6% to fund a 100%+ return project. The math works regardless of Fed policy.

This is new. Historically, when you raise rates, capex spending slows because the cost of capital goes up relative to returns.

But the cost of compute capital is now so low relative to returns that Fed policy is essentially irrelevant for AI infrastructure spending.

"All these hyperscalers were sitting on more cash together than the US Treasury had."

Translation: They don't need to borrow. They can fund everything from cash reserves.

The Bigger Picture: US Compute Export Economy

Tinsman and Bent are describing something larger:

America is building an economy around exporting compute processing power to the world.

"We're building data centers in the US and we're leasing it out to the rest of the world at like 90% profit margins."

"Our compute is serving the whole 7 billion people of the world... the scale of this is international."

This is reminiscent of:

- US oil refining dominance (20th century)

- US tech platform dominance (21st century)

- And now: US compute infrastructure dominance

The structural advantages:

- Cheap energy (Texas, friendly regulation)

- Existing tech infrastructure

- Capital availability

- Regulatory environment in red states favors data centers

This creates a multi-decade moat.

What This Means for Investors

The compute leasing revelation upends traditional valuation frameworks:

Data center operators aren't just building capacity. They're cash flow machines.

Current valuations of data center plays (CoreWeave, Digital Realty, Equinix, cloud service providers) likely undervalue the earnings potential because the market hasn't fully priced in 10x+ ROI economics on compute leasing.

Token demand growing 80x (Anthropic) + 24x more ahead (Goldman projection) = multi-year earnings visibility that should support higher multiples.

The Fed's rate policy is irrelevant for AI capex, meaning these investments are Fed-proof. They'll compound regardless of rate environment.

The Trade Structure

With conviction in the compute leasing supercycle:

AMD Bull Call Spread (Semiconductor Beneficiary)

- Structure: Buy $160 calls, sell $200 calls, 3-4 months out

- Max Profit: $4,000 per spread

- Max Loss: Premium paid (~$1,500)

- Breakeven: $175

AMD benefits from sustained AI capex and compute infrastructure buildout. Growth visibility is 2-4 quarters of earnings surprises ahead.

NVIDIA Iron Condor (Consolidated at Highs)

- Structure: Sell $920/$940 call spread, sell $820/$800 put spread

- Max Profit: Net credit (~$800-1,200)

- Max Loss: $2,000 minus net credit

- Breakeven: $801 and $939

NVIDIA is the foundational play but may consolidate after recent gains. Iron condor collects premium while theta works in your favor.

Oracle Synthetic Long (Software Enabler)

- Structure: Sell cash-secured puts at $135 strike

- Max Profit: Premium + upside above $135

- Max Loss: Assignment at $135 minus premium

- Breakeven: $135 minus premium

Oracle benefits from AI agent demand (multiple software subscriptions per agent). Generate income while building position.

The Bearish Signal Nobody's Talking About

Tinsman mentions a critical detail that should concern everyone:

Fertilizer prices are up 100%+ (nitrogen, phosphate, sulfur) while corn prices haven't kept pace.

This is a supply chain crisis hitting agriculture.

"John Deere refusing traditional financing to 40% of customers."

When a company with a 200-year history starts refusing financing, it signals credit stress in the customer base (farms).

This suggests farm income is compressed between input costs (fertilizer) and output prices (corn).

This could become a broader economic problem if agricultural stress spreads to rural credit and employment.

The Bottom Line

Tinsman and Bent are describing a structural breakdown in how monetary policy works:

- Compute leasing economics are 10x+ ROI — Data center operators aren't capital-intensive enterprises; they're cash flow machines

- Token demand is exponential — 80x growth already, 24x more to come (Goldman)

- Fed policy is irrelevant — When your ROI is 100%+ and you have $800B in cash, interest rates don't matter

- US compute export economy emerging — 90% margins, global customer base, multi-decade moat

- Infrastructure valuations likely underpriced — Market hasn't fully capitalized on earnings potential

- Agricultural stress building — Fertilizer costs squeezing margins; John Deere financing denial is a warning sign

The immediate implication: AI compute infrastructure plays are Fed-proof and offer asymmetric upside as token demand continues explosive growth.

The longer-term implication: The Fed has lost a critical tool for managing economic cycles when your biggest capex spenders are insensitive to rate policy.

Important Disclaimer

- This is analysis of a podcast conversation, not financial advice

- All trade ideas are hypothetical and educational

- Options strategies carry significant risk

- Valuation assumptions in this analysis may be incorrect

- Agricultural stress could spread faster than expected

- Supply chain disruptions could alter capex timelines

- Consult a licensed financial advisor before trading

- Past performance doesn't guarantee future results

Lisa Tamati reports on AI infrastructure, monetary policy, and market structure at PTLsignal.com

// newsletter

Want more like this?

Join the PTL Signal newsletter. Weekly AI, Bitcoin & market analysis from Lisa Tamati.